| W.I.L. Home Page | Finance Digest Home |

| Sign Up | Offshore News Digest Home |

HOW TO TRADE WITH THE TREND

There are four cardinal principles which should be part of every trading strategy. They are: (1) Trade with the trend, (2) Cut losses short, (3) Let profits run, and (4) Manage risk. You should make sure your strategy includes each of these requirements for success. Trade with the trend relates to the decision of how to initiate trades. It means you should always trade in the direction of recent price movement. Mathematical analysis of commodity price data has shown that these price changes are primarily random with a small trend component. This scientific fact is extremely important to those desiring to pursue commodity trading in a rational, scientific manner. It means that any attempt to trade short-term patterns and methods not based on trend are doomed to failure.

A good example of such a doomed method is Japanese Candlestick patterns. This theoretical conclusion is consistent with my previous research. Many years ago, just as Candlesticks came into vogue, I attempted to create a profitable trading system incorporating Candlesticks. I tried many patterns and many types of systems, all without success. I have never seen anyone else demonstrate the effectiveness of Candlesticks using objective rules either. Successful traders use a method that gives them a statistical edge. This edge must come from the tendency of commodity prices to trend. In the long term you can make money only by trading in synch with these trends. Thus, when prices are trending up, you should only buy. When prices are trending down, you should only sell.

While this important principle is well-known, traders violate it surprisingly often. They are looking for bargains so they prefer to try to buy at the very bottom or sell at the very top before new trends become established. Winning traders have learned to wait until a trend is confirmed before taking a position consistent with that trend. The alternative to trend following is predicting. This is a trap that nearly all traders fall into. They look at the commodity trading problem and conclude that the way to be successful is to learn how to predict where markets will go in the future. There is no shortage of people willing to sell you their latest prediction mechanism. We all want to believe that predicting is possible because it is so darn much fun to make a prediction and be right.

For the greatest chance of success, your time frame to measure trends should be at least four weeks. Thus, you should only enter trades in the direction of the price trend for the last four weeks or more. A good example of a trend-following entry rule would be to buy whenever todays closing price is higher than the closing price of 25 market days ago, and sell whenever todays closing price is lower than the closing price of 25 market days ago. When you trade in the direction of this long a trend, you are truly following the markets rather than predicting them. Most unsuccessful traders spend their entire careers looking for better ways to predict the markets. If you can develop the discipline to measure trends using intermediate to long-term time frames and always trade in the direction of the trend, you will make a giant step in the direction of profitable trading.

Link here.THIS CHART SAYS U.S. LONG BOND YIELDS ARE HEADING HIGHER

When I first started working as an economist for a large investment house, I foolishly ridiculed my older colleagues fascination with charts and technical analysis. Several humbling experiences later it dawned on me that (trying to) listen to what the markets were saying might not be a bad idea. This chart of U.S. long bond yields seems to me to be speaking very loudly indeed.

In a previous column, I disagreed with then bond bullish views of Pimcos Bill Gross he seems to have changed his mind somewhat in his April Investment Outlook and set out a bearish fundamental case on bonds. The bear case has recently received strong support from bond price developments. The chart is a technically alarming one for bond bulls. Firstly, the long term trend as shown by the two year moving average is strongly upwards. Secondly, yields have decisively broken up through very strong resistance between 4.40% and 4.60%. Thirdly, yields have also broken through the 12-year downtrend obtained by joining the peak levels attained in 1994 and 1999. My reading of this chart is that U.S. 10-year bond yields are likely to move up to test the next major resistance at around 5.40% to 5.60%, as represented by the peaks in 2001 and the low of 1995. This is a medium term expectation rather than a short term one.

Could the fundamentals justify such a back up in yields? I believe they can. Americas huge and growing dependence on foreign capital means that it may face both a slowing economy and higher interest rates. In this respect the recent decision by Congress to block Arab ownership of some U.S. ports may prove extremely counterproductive. Further rises in U.S. long bond yields would of course be unhappy news for the U.S. economy, and for equity and real estate markets.

Link here.THE SLIPPERY SLOPE

The U.S. Congress is working overtime on protectionism. As one senior Washington insider confided to me the other day, concerns over China are boiling over in this town. While extreme actions on the tariff front have been deferred at least for the moment it is starting to look as if an even bigger train has left the station. The angst of worker insecurity is proving to have irresistible bipartisan appeal within the American body politic. The odds are rising that Washington will enact some form of protectionist legislation before the mid-term elections this November. The dangerous slide down a slippery slope has begun.

The good news is that Senators Schumer and Graham have elected once again to defer a floor vote on their proposal for a so-called currency-equalization tariff of 27.5% that was to be levied on all Chinese imports into the U.S. a surcharge they believe would provide fair compensation for an undervaluation of the RMB by a like amount. My guess is that this type of extreme legislative action has now fallen out of favor in Washington. In its place, a less contentious but very hard-hitting legislative option has now emerged The United States Trade Enhancement Act of 2006 (USTEA06) proposed by Senators Grassley (R-Iowa) and Baucus (D-Montana), the Chairman and ranking minority member of the all-powerful Senate Finance Committee. Unlike the Schumer-Graham proposal, this bill also appears to be far more palatable to the Bush Administration. In congressional testimony on 29 March, the Grassley-Baucus option was praised by senior officials from the U.S. Treasury, the Department of Commerce, and the office of the U.S. Trade Representative. This could well represent a sea change in the politics of trade legislation a bipartisan proposal with White House support.

In a nutshell, USTEA06 rewrites the book on how the U.S. both identifies and responds to external imbalances and currency misalignments the latter word being a deliberate and important substitute for the oft-contentious characterization of manipulation that has long plagued the foreign trade debate. The Grassley-Baucus bill empowers a new office in the U.S. Treasury to develop a more sophisticated set of tools to identify those nations guilty of misalignments, and it establishes a consultation mechanism with the IMF and the U.S. Trade Representative to arrive at this determination. Should a verdict of misalignment be rendered, USTEA06 offers a broad arsenal of remedial actions to be directed at the offending nation.

Meanwhile, the U.S. Senate Banking Committee is hard at work on another track a major revamping of the approval process for cross-border M&A transactions into the U.S. This proposal owes its origins to two highly politicized, and eventually scuttled, foreign takeover attempts last years proposed Chinese acquisition of Unocal and the recent Dubai Ports fiasco. Like the Schumer-Graham and Grassley-Baucus trade and currency initiatives, the Shelby proposal enjoys broad bipartisan support. The bottom line is that new sources of friction are being added to cross-border M&A activity in the U.S.

These two seemingly disparate strains of Congressional activity directed at currency- and foreign-investment-related concerns have one important thing in common: They are both examples of a dangerous combination of election-year politics and bad economics. In particular, politically-driven constraints on trade and capital flows run very much against the grain of the foreign funding imperatives of a saving-short U.S. economy. Lacking in domestic saving, America is more in need of foreign capital than ever before and, of course, must run massive current-account and trade deficits to attract that capital. By throwing sand in the gears of trade and capital inflows precisely the effects of the two proposals Americas external funding problem can only get thornier. Downside risks to the dollar and upside risks to real long-term U.S. interest rates are a growing concern in such a climate.

Washington politicians are making an especially serious mistake by focusing on the China problem in isolation from these broader macro concerns. A reduction of a bilateral trade deficit with one nation will do nothing to resolve what is truly a multilateral problem for a saving-short U.S. economy. The water balloon analogy applies all too well in this instance. Until or unless the U.S. fixes its saving problems and reduces its claim on the pool of foreign saving, a reduction in the Chinese bilateral deficit will only shift that portion of the shortfall elsewhere. The same line of reasoning basically follows with respect to the initiative on foreign takeovers. If those flows are impeded, the external funding will then need to be sourced through a different channel. To the extent those incremental inflows get redirected into portfolio flows either stocks or bonds it would not be unreasonable for foreign investors to seek concessions on the terms by which those funds are provided. That could well imply a weaker dollar and/or higher real interest rates outcomes that could, in turn, spell serious trouble for the U.S. economy. Here, as well, by failing to address the root cause of Americas external imbalance an unprecedented shortfall of domestic saving Washington could be blindsided by the unintended consequences of the water balloon effect.

Trade has become the economic lightening rod in this political season. If anything, the pressures for legislative action will only intensify between now and the mid-term elections in early November. Within the Congress, support for action is bipartisan and deep. A politically weakened White House is unlikely to buck the tide. All in all, politicians who are soft on trade will be characterized as unsupportive of the plight of the beleaguered American middle-class wage earner. With the political fix increasingly at odds with the macro fix, the odds of a disruptive U.S. current account adjustment are rising.

Link here.THE GREAT GLOBAL GROWTH DEBATE

The global growth debate could well prove decisive for financial markets in 2006. An increasingly synchronous and vigorous acceleration in world economic activity has been evident in the early months of this year. With the markets now discounting the likely persistence of this synchronous boom, it pays to ponder whether the global growth story might swing the other way.

There can be no mistaking a decisive acceleration of the world economy in early 2006. A quarterly global GDP proxy maintained by Morgan Stanleys global economics team now points to a 3.4% annualized gain in industrial world GDP in 1Q06 fully 70% faster than the anemic 2.0% pace recorded in 4Q05. Within the developed world, the acceleration was particularly evident in the U.S., although the latest calculation of 1Q06 real GDP growth in the U.S. is not nearly as vigorous as we had once thought would be the case. In Europe, the degree of acceleration is equally impressive although the absolute growth rates continue to fall well short of those evident in the U.S. Particularly impressive was a sharp increase in German business sentiment in March. Taken literally, the latest European business surveys underscore upside risks to our upwardly revised growth estimates for 1Q06. They also hint at the possibility of a spillover of the newfound vigor into the spring quarter. In Japan quite possibly the worlds most exciting economic recovery story our estimates suggest the economy slowed to a more sustainable 2.9% clip in 1Q06 still a very impressive gain for an economy that had been mired in a 1% growth slump for well over a decade.

In the developing world, quarterly data on economic activity are highly unreliable. But in tracking the ongoing pace of the global economy, we take a stab at estimating sequential quarterly growth patterns in their respective regions, as well. Our latest take from this exercise points to a bit of a slowing in 1Q06 relative to exceptionally vigorous gains evident in 4Q05. I would not place much weight on the quarter-to-quarter volatility but would, instead, underscore the average 6.5% increase over that two-quarter period more than twice the pace we estimate for the industrial world (2.7%) over that same interval. With the developing world accounting for 45% of world GDP, as measured by the IMFs purchasing power parity metrics, this ongoing vigor can hardly be taken lightly.

Financial markets time horizons have shortened as the momentum play has taken center stage in the debate. Periodic growth scares, as well as equally frequent boom alerts, are all too frequent by-products of this ever-myopic culture. The current verdict is very much on the boom side of the global growth call. The recent back-up in long-dated sovereign yields is an important case in point. In the U.S., e.g., the increase in 10-year Treasury yields toward the all-important 5% threshold a level that has not been seen in nearly two years is almost exclusively traceable to a surge in the real interest rate component. As measured in the TIPS market, real yields are close to a 3-year high suggesting that the bond market could well be close to maxing out on its perceptions of growth risks. The inflationary premium, by contrast, has changed very little over the same period. The connection between financial markets and the growth implications of the latest spin of the incoming data flow has never seemed tighter.

Yet as night follows day, the global growth story has its own inevitable ebbs and flows. Based on our quarterly global growth proxy, our baseline forecast implies that industrial world GDP growth in 1Q06 probably hit its high-watermark for at least the next couple of years. If we are right, that means financial markets will need to start factoring in at least a modest deceleration. The risk, in my view, is that any such slowing could be far more pronounced than our current baseline implies. Three considerations lead me to that conclusion the first being a post-housing-bubble capitulation of the over-extended American consumer. As the housing bubble continues to deflate and equity extraction from property fades, I continue to believe that income-constrained American consumers will prune discretionary spending. China could well be a second source of deceleration over the course of this year, as the government makes a downpayment on its avowed rebalancing away from exports and fixed investment toward private consumption. Rising protectionist risks could well provide a third source of deceleration (see article summary directly above).

Financial markets are currently dismissing downside growth risks leaning the other way betting more on the upside of the global momentum play or, at worst, believing that any deceleration in the pace of world activity is likely to be minimal. In my view, that leaves markets increasingly exposed on the other flank to the possibility of a downside growth surprise. If those risks play out, bonds could rally and equities could sag on growth concerns. The biggest risk, however, is that it does not take all that much to turn the global liquidity cycle. For their part, the worlds major central banks are all on the tightening side of the monetary equation for the first time in 15 years. If the turn in the global liquidity cycle reinforces a downshift in global growth, financial markets could be especially vulnerable.

Recent action in some of the more exotic corners of the markets may well be providing a hint of how that vulnerability might spread. An unwinding of carry trades in Iceland and New Zealand, corrections in Middle Eastern equity markets, and very recent pullbacks in commodity-linked currencies (i.e., Canada and Australia) could well be canaries in a much bigger coal mine. Even the big equity markets in the U.S., Europe, and Japan have looked a bit toppy in recent days as yields on long-dated U.S. Treasuries close in on the 5% threshold.

The global economy has just come off a very hot and increasingly synchronous burst of growth. Momentum-driven financial markets are betting this trend will continue. However, there is good reason to suspect that the ever-fickle pendulum of global growth is now about to swing the other way. If that turns out to be the case, myopic markets could reverse course in a flash.

Link here.HOUSING BUBBLE TROUBLE

If something cant go on forever, it wont. ~~ Herb Stein

With new home sales down 10.5% in February, and with home prices declining for the fourth month in a row, it is high time for a sober look at the consequences of a major housing correction. The Federal Reserve, Wall Street economists, and other observers of the U.S. economy are closely watching the housing market because it has been a key driver of economic growth over the past several years. Roughly a quarter of the jobs created since the 2001 recession have been in construction, real estate, and mortgage finance. Even more important, consumers have withdrawn $2.5 trillion in equity from their homes during this time, spending as much as half of it and thus making a huge contribution to the growth the U.S. economy has enjoyed in recent years (consumer spending accounts for two-thirds of GDP).

But consumers cannot keep spending more than they make. Eventually, home prices will flatten, the flood of cash out refinancings will become a trickle, and consumer spending will slow, as will job creation in housing-related industries. The big question is this: Will the housing sector experience a soft landing and slow the economy or a hard landing that pushes us into recession? Countless articles in the financial and popular press have now been devoted to the question of whether we are in a housing bubble. It is a favorite topic of many liberal economists, columnists, and bloggers, who argue that President Bushs tax cuts and other policies have created a hollow and unsustainable economy. They are laying the groundwork to hang a housing bust around the necks of President Bush and congressional Republicans.

Economic observers on the right have been strangely silent on this debate. A few conservatives have argued that the record appreciation of home prices is justified by economic fundamentals. Others, who apparently slept through the 80% decline in the NASDAQ, do not believe bubbles are possible in a free market economy. Certainly most conservatives have an innate optimism about America and the resilience of its free market economy, and a strong and well-justified aversion to doomsayers. And naturally, the White House and congressional Republicans have no interest in highlighting the vulnerabilities of the economy.

Yet the concerns about unsustainable growth in consumer debt and home prices are not easily dismissed. The crux of the debate is house prices. If the inflated prices are justified by economic fundamentals and sustainable, then the 82% increase in mortgage debt since 2000 will probably turn out to be innocuous and the risks to the economy minimal. If, on the other hand, prices are out of whack, painful adjustments lie ahead. Unfortunately, the weight of the evidence strongly suggests a bubble. The price of the median home is up an inflation-adjusted 50% during the last five years, an unprecedented national increase.

Just as cheerleaders of the high-tech bubble of the late 1990s developed ever more creative explanations for why traditional metrics of valuing stocks no longer applied, the same has been true during the housing bubble. Housing bulls point to immigration, building restrictions, Baby Boomer demand for second homes, and other seemingly plausible justifications for skyrocketing home prices. But examining the value of housing using time-tested and common-sense metrics such as price-to-income and price-to-rent ratios suggest the gains in the bubble areas cannot be explained by economic fundamentals. Consider the price-to-income ratio, an obvious measure of affordability. This ratio has reached an unprecedented level in the bubble markets. While this ratio hovered around its average of 4-to-1 for the past 30 years, it has zoomed to nearly 8-to-1. An even better indicator of how divorced home prices are from their underlying economic value is the price-to-rent ratio. In the Washington, D.C., metro area, which had remained relatively constant for several decades, this ratio has soared since 2000. If this is not a housing mania, why have so many people embraced financing schemes that leave them vulnerable to higher interest rates or even a modest correction in home prices?

Link here.The menace of an unchecked housing bubble.

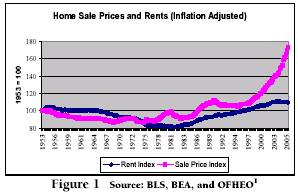

An unprecedented run-up in the stock market propelled the U.S. economy in the late 90s and now an unprecedented run-up in house prices is propelling the current recovery. Like the stock bubble, the housing bubble will burst. Eventually, it must. When it does, the economy will be thrown into a severe recession, and tens of millions of homeowners, who never imagined that house prices could fall, will likely face serious hardships.

The basic facts on the housing market are straightforward. Quality-adjusted house prices ordinarily follow the overall rate of inflation. However, in the last eight years house prices have risen by almost 50% in real terms, as shown in Figure 1. The run-up has not been even. In large parts of the country (most of the South and Midwest) there has been little real appreciation in house prices. In contrast, the runups in the bubble areas (the West Coast, the East Coast north of DC, and Florida) have been close to 80% in real terms.

The housing bubble spurs the economy directly by increasing home construction, renovation, and sales and indirectly by supporting consumption. The run-up in house prices has created more than $5 trillion in real estate wealth compared to a scenario where prices follow their normal trend growth path. The wealth effect from house prices is conventionally estimated at 5 cents on the dollar, which means that annual consumption is approximately $250 billion (2% of GDP) higher than it would be in the absence of the housing bubble.

Nobody doubts that there has been a sharp increase in house prices, the question is why: Is it because of fundamentals or a speculative bubble? A quick examination of the fundamentals should remove any doubts on this issue. On the demand side, neither income nor population growth has been especially rapid. Real per capita income has grown at a respectable rate of 2% annually since 1997, but this is considerably slower than the 2.8% annual rate from 1953 to 1973, a period which saw no run-up in house prices. Furthermore, the median family income has actually been falling since 2000. Population trends also would not suggest a surge in demand for housing. There also is no obvious supply-side story. The best evidence that fundamentals are not the cause of the run-up in housing prices is the fact that there has been no comparable increase in rental prices. The fact that only the ownership market shows an unusual run-up in prices strongly supports the view that this price increase is being driven by speculation rather than fundamentals.

If housing prices are a speculative bubble, then eventually, prices will return to normal levels reflecting the value of housing services. The country has been building houses at a near record pace for the last few years, and this pace will continue as long as prices remain near their bubble peaks. At the moment, this oversupply has been absorbed by speculators and by a record vacancy rate in the rental market, but eventually excess supply will put downward pressure on sale prices (part of this story is the conversion of rental property to ownership units), which will cause speculative demand to evaporate. Just as the supply of shares of worthless Internet companies eventually outstripped demand, the supply of housing will eventually place enough downward pressure on housing prices that the bubble levels will prove unsustainable. The adjustment process will not be pretty.

Link here.Some homeowners struggle to keep up with adjustable rates.

Americas 5-year real estate boom was fueled partly by a tempting array of cut-rate mortgages that helped millions of Americans qualify for home or refinance loans. To afford soaring home prices, many turned to adjustable-rate and other, riskier loans with low initial payments. The homeownership rate hit a record 70%. Now, the real estate market is cooling, interest rates are rising and tens of thousands more Americans are starting to have trouble paying their mortgages. Nearly 25% of mortgages 10 million carry adjustable interest rates. And most of them went to people with subpar credit ratings who accepted higher interest rates, according to the Mortgage Bankers Association. Within the last year, I would say 60% to 70% of calls to our hotlines are issues related to ARM (adjustable-rate mortgage) loans, says Chris Krehmeyer, executive director of Beyond Housing, a non-profit group that offers homeownership support services in St. Louis. Thats significantly higher than in years past, because the ARMs are coming home to roost.

Last week, the Federal Reserve raised interest rates for the 15th time since June 2004 and signaled that at least one more increase is likely. That trend is ominous for borrowers who were seduced by adjustable-rate loans that offered interest-only payment options or teaser rates below 2% or that let the borrower pay less than the interest owed. They will face bigger payment shock once their loans reset to higher rates. The number of borrowers in trouble will rise this year and peak in 2007 and 2008 as the largest number of mortgages reset to higher rates, according to First American Real Estate Solutions, a real estate data provider. Already, in West Virginia, Alabama, Michigan, Missouri and Tennessee, about one in five homeowners with a high-interest (subprime) ARM was at least 30 days late at the end of last year, according to the Mortgage Bankers Association. After 90 days, the foreclosure clock starts ticking. Most of those foreclosures are related to job losses in auto and garment factories. Higher mortgage payments were often the last straw.

What worries experts such as Christopher Cagan at First American Real Estate Solutions are the adjustable-rate loans made in 2004 and 2005, at the end of the housing boom. These loans were concentrated in the hottest markets, such as California, where about 60% of all loans last year were interest-only or payment-option ARMs the highest such rate in the country. Of the 7.7 million households who took out ARMs over the past two years to buy or refinance, up to 1 million could lose their homes through foreclosure over the next five years because they will not be able to afford their mortgage payments, and their homes will be worth less than they owe, according to Cagans research. The losses to the banking industry, he estimates, will exceed $100 billion. That is less than the damage from the savings-and-loan crisis in the 1990s, which cost the country $150 billion.

There are a few resources to help homeowners in dire financial straits. The Homeownership Preservation Foundation offers free credit counseling and referrals, 24 hours a day, seven days a week (888-995-4673). And NeighborWorks America, a national non-profit that supports homeownership and financial literacy, has member groups in every state. One of its members, Neighborhood Housing Services of Chicago, has been receiving about five calls a day since January from borrowers who are falling behind on ARMs.

Link here.Residential construction lending at troubling levels, FDIC says.

Nearly three out of four of Atlanta-based banks are heavily weighted in construction and development loans and could face trouble if the housing market continues to cool. 87 of the 118 banks with headquarters in Atlanta have high concentrations of construction and development (C&D) loans the vast majority for residential projects according to the Federal Deposit Insurance Corp. The FDIC, along with three other regulating agencies, has proposed new guidelines amid concerns over real estate lending concentrations nationally. The agencies recommend that banks should have robust risk management practices if more than 100% of their capital is exposed to construction and development projects. Banks use deposits and borrowed money from other sources to make loans, allowing them to lend well in excess of their capital.

Atlanta banks are significantly more invested in real estate than they were during the last real estate downturn. In 1991, only 29% of Atlanta banks, versus 74% today, had C&D loans totaling more than 100% of their capital. In fact, the metro areas banks have the greatest median C&D loan-to-capital ratio among the nations top 10 residential construction markets. Las Vegas, No. 2 on the list, has a median C&D loan-to-capital ratio of just 180%, versus Atlantas 265%. Observers say Atlanta banks reliance on C&D lending is a function of demand in one of the hottest housing markets in the U.S. Local bankers say C&D lending remains a good and abundantly available bet. And, they say they have risk management controls in place to make sure those bets do not go bad if the housing market continues to cool.

Link here.Foreclosure shock hits Denver market.

Rising interest rates, a glut of unsold homes on the market and falling home prices in some submarkets drove up Denver-area real estate foreclosures by more than 30% in the first quarter of this year compared with the first three months of 2005. The 31.5% jump is the largest year-over-year percentage increase for a quarter in almost two years. The jump to 4,764 foreclosures compared with 3,624 in the first three months of 2005 took some experts by surprise. Public trustee offices in Adams, Arapahoe, Boulder, Broomfield, Denver, Douglas and Jefferson counties estimated the number of foreclosures they expect to open this month.

That is disturbing, said economist Patty Silverstein, principal of Development Research Partners, of the soaring number of foreclosures. We still expected to see increases in 2006, but this is larger than what I would have expected. At this point in our economic recovery, we would have expected to have seen a smaller increase in foreclosures. She said that a main culprit appears to be interest-only and other variable-rate loans that homeowners have taken out in huge numbers in recent years to reduce their monthly mortgage payments. A lot of people have taken out these different types of mortgage products during the past couple of years, and now people are discovering that their payments are starting to ratchet upward with rising interest rates.

Sean Healey, the broker-owner of Keller Williams Preferred Realty, said he was not surprised by the number of foreclosures and believes the market has a couple of years of pain ahead. What I see is not pretty, said Healey, who also heads the Healey Group and hosts a radio talk show called The Real Estate Advocate. He said the number of unsold homes on the market has been growing by an average of 2.5% a week. The increasing supply is putting downward pressure on sale prices, especially for the lower-priced homes most likely to go into foreclosure. That is a vicious cycle because it forces more sellers to lower their prices, driving even more houses into foreclosure, Healey said. Primarily, I see a huge glut of homes priced under $300,000. Under $200,000, it is just a blood bath, a path of devastation. It is just ugly. In some areas of Adams County, sellers of lower-priced homes are finding that the market value of their home is down 15% to 17% from what they paid a couple of years ago, Healey said. Economist Tucker Hart Adams said that foreclosures are a lagging indicator and will continue to rise even as the economy gets back on its feet.

Link here.Investors helped to fuel housing boom.

U.S. home sales would have been little changed in 2005 had it not been for investors, who were lured by price increases that soared as much as 49% in some regions of the country. As sales of new and existing houses rose 4.6% to 8.36 million, investment purchases represented 28% of the total, up from 25% in 2004, according to data released by the National Association of Realtors in Washington, D.C. Excluding investments, sales rose 0.9% to 5.99 million.

nvestors seeking alternatives to stocks helped fuel the housing boom by competing for property and bidding up prices, prompting former Federal Reserve Chairman Alan Greenspan to warn of froth in the real-estate market. Rates for the adjustable loans favored by investors climbed about 1 percentage point as the Fed raised its benchmark rate eight times last year. The bulk of the decline in home sales this year will come from investors leaving the housing market, said David Berson, chief economist of mortgage buyer Fannie Mae. If home price gains have peaked, as we expect, and financing is more expensive, investors are going to find someplace else to put their money. Home sales probably will decline 8.9% to 7.61 million this year, Berson, 51, said. The average rate for a 30-year mortgage that adjusts annually likely will increase to 5.44% from 4.48% last year, he said.

Home prices, which rise about 5% a year on average, gained 12% to $208,300 in 2005, the biggest jump in 26 years, according to NAR data. Investment properties, which are resold without the buyers ever living in them, had price appreciation of 24% last year. Sales of vacation homes, which are used by purchasers as a second home and sometimes rented, rose 17% from a year earlier to 1 million, the brokers group said. The price of vacation homes climbed 7.4%, according to the report.

Link here.Vancouver too bubbly?

The Western Canada housing market remains on fire, with Vancouver displaying the greatest bubble-like qualities, a Toronto-Dominion Bank report said. Overall, Canadas housing market reflects a tale of regional divides, with the West still strong while central and Atlantic Canada appears to be cooling, TD said. Across the country, house prices jumped almost 10% in the first quarter, with sales and new-home construction also remaining strong.

While much of the growth in the West has been supported by strong economic fundamentals and the level of affordability does not suggest that housing in Victoria, Edmonton, Calgary, Saskatoon or Winnipeg has become frothy, the risk of speculative pressures is present, TD said. It sees those risks as particularly acute in Vancouver. Vancouver has the greatest bubble-like qualities, with prices rising at a 22-per-cent annual pace in the first quarter of 2006, average home prices reaching close to half a million dollars and affordability deteriorating to the worst level in the country.

Link here.RISING RATES PINCH CONSUMERS

The recent uptick in long-term interest rates may signal that the end of a long period of cheap credit is at hand. That means the economy is humming, but what would higher interest rates mean for consumers? Government statistics show that consumer spending levels have been higher than income levels for years, prompting economic worrywarts to conclude that an eventual slowdown in consumer spending levels is inevitable. If interest rates make a sustained move to the upside now, that thesis will be put to the test. The employment market is healthy, but consumer liquidity, which has been supporting consumer spending growth above the level of income growth, is drying up, says Colin McGranahan, a retail analyst with Sanford C. Bernstein. A steepening yield curve only accelerates that. It makes me think that this might push down on the consumer spending deceleration button in the coming months.

The yield on the 10-year Treasury note was recently hovering near 4.9%, a level it has not reached in almost a year. Some investors say it is headed for 5%, which would mark its highest level since 2002. For most of last year the yield on the 10-year stayed at 4% to 4.5%, even while the Federal Reserve moved short-term rates into that range. Normally, such a move by the Fed would goose longer-term rates higher, because bond buyers typically demand a higher rate of return for a longer time horizon on their investments. When this did not happen, now-retired Fed Chairman Alan Greenspan famously called the situation a conundrum.

The plot thickened late last year when short-term rates climbed higher than long-term rates, creating an inverted yield curve. Inverted yield curves have, in the past, signaled the onset of an economic recession. This time around, Greenspan voiced the widely held opinion that foreign demand for long-term U.S. bonds was pushing down long-term rates, so the inverted yield curve was not a sign of an economic slowdown. So far, the Greenspan crowd has been right. Now long-term rates are moving up again, prompting some observers to conclude that, rather than heading for a slowdown, the economy is heating up and the increase in long-term rates is only the beginning. The low-interest rate cycle that really began in 1982 but has gone to extremes in the last four years may be coming to an end here, says Paul Mendelsohn, chief investment officer with Windham Financial Services. Gold is telling us that. Commodity prices are telling us that. It looks like the dollar may be getting ready to tell us that. You have a developing set of circumstances that could send interest rates up quite a bit.

Link here.The consumer crunch: An update on cash flow, debt, real estate and money supply.

The longer that we research the U.S. economy, the easier it gets. We have learned the accounting ins and outs. We have tracked the principles of misleading accounting consolidations from Enron to the GDP. We have accepted it all and we know how to follow it. This analysis brings our Consumer Cash Flow, Real Estate and Money Supply, and The Interest Rate Conundrum papers up-to-date. In simple terms, the U.S. economy has become completely dependent on consumer and government debt creation. We will track the consumer side effects and show them in the consumer accounts.

The information shows that U.S. households were experiencing increasing financial stress during the second half of 2005. The liquidity characteristics of this distress are also increasing. Interest rate levels do not currently allow any respite. They have entered the zone where positive financing outcomes are hard to achieve. 2006 is the year when the consumer could hit the wall. Consumer cash flow is not high enough to support increasing debt and spending levels without increasing levels of debt flow. Interest rates are now restraining consumer debt flow and the liquidity side effects could become obvious as early as this spring. Our papers have previously identified the process and this paper updates the information and conclusions from those papers.

Link here.RETIREMENT: GREAT EXPECTATIONS, NO PREPARATION

Cognitive Dissonance 101 might be a fitting title for the findings from the 2006 retirement confidence survey released Tuesday by the Employee Benefit Research Institute. Here is just one example: A quarter of workers participating in the survey said they were very confident about their prospects for financial security in retirement, and another 44% said they were somewhat confident. But among those in the very confident group, 22% said they are not currently saving for retirement and 39% said they have less than $50,000 in savings. Of course, low savings are not the exclusive domain of the overconfident. 65% of all workers said they had less than $50,000 in total savings and investments, not including the value of their home or any defined-benefit pension they may receive.

While older workers tend to have more assets than younger workers, the EBRI survey found that 58% of workers between ages 45 and 54, and 56% of those age 55 and older had less than $50,000 in savings. Nevertheless, 59% of all workers say they would like to enjoy a standard of living in retirement that is the same or better than the standard of living they have in their working years. But half the respondents think they can manage that on 70% or less of their pre-retirement income. That does not square with financial experts recommendation that you should plan to live on at least 70% of your pre-retirement income. Nor does it square with the 55% of present-day retirees surveyed who said they live on 95% or more of their pre-retirement income.

Then there is the disconnect between what workers expect to receive in terms of pension and healthcare benefits and the fact that companies increasingly are freezing their pension plans and modifying or eliminating healthcare benefits. 61% of workers said they expect to receive pension benefits in retirement, even though 40% say they do not currently have a pension plan. 37%, meanwhile, said they think their employers will provide health benefits in retirement. More troubling, though, is that regardless of whether a worker expects to receive healthcare benefits, there is no difference in the amount of income he expects to need in retirement. Yet Fidelity estimates that the average couple retiring this year will need $200,000 to cover their healthcare costs alone for 20 years in retirement. And that does not include long-term care costs.

Part of the problem, for Baby Boomers anyway, is that the reality of retirements price tag has not hit them yet because they see their parents with adequate funds in retirement thanks to pensions and employer-provided health coverage, said EBRI fellow Jack Vanderhei. And they may figure that because they make more than Mom and Dad ever did, that they will be fine, too, he said. But Vanderheis research suggests that some Boomers will burn through a significant portion of their savings within 10 to 15 years of retirement as they try to maintain their current lifestyle.

Links here and here.CRITICS PUSH TO EASE PARTS OF SARBANES-OXLEY ACCOUNTING REFORM LAW

Critics of the Sarbanes-Oxley law to tighten U.S. accounting rules are taking their case to Congress, beginning a push to ease parts of the legislation enacted after the collapse of Enron and WorldCom. Republican Representatives Tom Feeney of Florida and Mark Kirk of Illinois and Democrat Gregory Meeks of New York will tell a House Government Reform subcommittee that the law has driven up company compliance costs, threatening small businesses in particular. The lawmakers have conducted a three-month listening tour, talking to chief executive officers, entrepreneurs and investors. At this point, there is an increasing recognition that the application of Sarbanes-Oxley has created some unexpected and unintended problems, Feeney said in an interview.

The hearing is the first in Congress that focuses on revising the law, which was named for its chief sponsors and was passed in 2002 with almost no opposition after Enrons bankruptcy and other scandals. Opponents claim the law has stifled innovation by putting burdensome regulations on companies. Sarbanes-Oxley set up a new system of regulation for the accounting industry, required top corporate officials to certify that their company books were in order and increased penalties for corporate fraud. A study last month estimated North American companies would spend $6 billion this year to comply with the law. But a study of 47 companies by Compliance Week found median compliance fees paid to outside auditors under the law were 0.6% less in 2005 than the previous year. The median decline in overall accounting fees was 7.4%.

Link here.SEVEN TRENDS SPELL A U.S. FINANCIAL CRISIS

Right now we face some powerful negative forces that could lead to a dollar panic, a stock market crash, or a banking crisis, said Investment U Chairman Mark Skousen in a lecture recently at Columbia University. The basis of my remark, says Skousen, is a warning issued by none other than former Fed Chairman Paul Volcker. A year ago he warned that The U.S. is skating on increasingly thin ice. The circumstances seem to me as dangerous and intractable as any I can remember, and I can remember a lot.

Whether that thin ice breaks, cracks or holds, says Skousen, depends on seven trends that are driving the U.S. economy. Its a medley of economic woes, he says, that include: (1) An overreacting Fed, switching from easy money to tight money. (2) Inflation and structural imbalances. (3) Poor consumer/investor finances. Our government policies promote overspending and undersaving on a massive scale. (4) A vulnerable financial/banking system. (5) Trade deficits and out-of-balance capital flows. (6) Overburdened federal debt levels, unfunded liabilities and rising interest rates. (7) The rising cost of war/natural disasters.

Its easy to get carried away with disaster scenarios, says Skousen. Dont ignore the fact that the stock market is currently at a four-year high. The single indicator I use to monitor global instability is the price of gold. If it spikes upward, were in trouble.

Link here.LIFTING RATES IN 2000, FED KNEW OF MARKET RISK

In May 2000, the Federal Reserve raised its main interest rate by the most in five years, even as its chief forecaster warned of the economic consequences of a possible stock market collapse. What lies ahead is certainly less attractive than the landscape of the past few years, Michael Prell, former head of the Feds research and statistics division, said in a May meeting on interest rates, according to transcripts for 2000. The record of exchanges between Alan Greenspan, then Fed chairman, and his colleagues provides a window into the Feds thinking as central bankers tried to slow an economy that had grown by more than 4% for three consecutive years.

The transcripts show Fed officials grappling with how to raise interest rates without putting too many people out of work or threatening the stock market. When weve attempted to apply the brakes in past expansions, we generally ended up skidding into a ditch, Mr. Prell said at the May 2000 meeting. Mr. Prell also said that in the current cycle, there would seem to be a risk of a particularly large decline in the market, given that, by many conventional metrics, we experienced a speculative bubble of extraordinary proportions. Mr. Prell is now a private consultant. The Fed raised its benchmark rate by half a percentage point at that time, to 6.5%, the sixth increase in eight meetings.

By March 2001, the economy was in recession after a 64% decline in the Nasdaq composite index and a 25% drop in the Standard & Poors 500-stock index in the previous 12 months, and the Fed was cutting rates at the fastest pace in Mr. Greenspans tenure. In December 2000, after data showed that the economy had expanded in the third quarter at the slowest pace in four years, Fed policy makers began to openly debate whether the economy would slide into a recession. The Feds rate committee voted unanimously that month to say that economic weakness was now a bigger threat than inflation, a signal that a rate reduction would come soon.

The Feds response to the stock market bubble is still a topic of debate. Mr. Greenspan has said on several occasions that the Fed should cushion the effect of bubbles rather than pop them and risk wider damage to the economy. The current chairman, Ben S. Bernanke, shares that view.

Links here and here.BERNANKES YIELD-CURVE CONFUSIONS

In his speech on March 20 the new Fed Chairman Ben Bernanke admitted that he is not so sure whether the Fed should be tightening its stance further or whether the central bank should pause. The reason, according to Bernanke, is the unusual behavior of long-term interest rates. Despite a visible increase in the federal funds rate from 1% in June 2004 to the current figure of 4.75%, the yield on the 10-year T-Note rose only slightly. At the end of March the yield stood at 4.74% against 4.58% at the end of June 2004. The Fed Chairman has concluded that the consequent narrowing in the spread between the long-term and the short-term interest rates (flattening in the yield curve) may imply that the present interest rate stance of the U.S. central bank is either too easy or too tight. It all depends, he says, on the type of expectations that investors hold.

According to Bernanke, there is a possibility that the premium on long-term interest rates may have fallen. Now, if this is the case then this could mean that investors expect an improvement in the future economic environment more stable inflation and a reduction in economic volatility. This is likely to set the platform for stronger economic activity in the months ahead. Hence, in his view and contrary to past experience, the present narrowing in the spread between the long-term and the short-term interest rates is likely to stimulate aggregate demand. Stronger economic activity in the months ahead, according to this way of thinking, means that the Fed must be more watchful as far as inflation is concerned. All this in turn implies that the Fed ought to maintain its present tight monetary stance.

Bernanke also raised the possibility that the narrowing in the yield spread could be due to expectations that short-term interest rates are likely to fall in the future as a result of a possible economic slowdown or a recession. If this is the case, the U.S. central bank should not proceed with its present tighter interest rate stance. The Fed chairman does not however assign very high likelihood to this scenario because both short- and long-term rates are relatively low by historical standards. To confuse things further, Bernanke has suggested that the real interest rate, which is consistent, with a stable economy (also known as the neutral interest rate) may have declined. Bernanke attributes the possible fall in the neutral rate to the world glut of savings, among various other causes. Now if this is correct, the current level of the fed funds rate may be too high. This means that the Fed should reverse its tight stance to prevent deflationary pressures.

Observe that for Bernanke whenever the federal funds rate is below the neutral rate this generates inflationary pressure since aggregate demand exceeds aggregate supply at the lower federal funds rate. Conversely, whenever the federal funds rate is above the neutral rate this sets in motion downward pressures on the prices of goods since at a federal funds rate above the neutral rate aggregate supply exceeds aggregate demand.

Historically since the 1950s the narrowing in the differential between the 10-year and the three-month Treasury note preceded most recessions in the U.S. This narrowing in the spread has occurred many months before the onset of the recession. Whenever the Fed reverses its monetary stance, which manifests itself through the change in the shape of the yield curve, the effect of this change in the stance does not assert itself immediately on the entire economy. The effect of a change in monetary policy shifts gradually from one market to another market. It is this that prompts the change in the shape of the yield curve to be seen as a leading indicator of economic activity.

Notwithstanding Bernankes view, we can conclude that the currently observed flattening or near inversion of the yield curve is an indication of a tighter Fed stance that is likely to undermine various activities that sprang up on the back of the previous easy monetary policy. In short, a flattening or the inversion of the yield curve is likely to result in an economic slowdown. Our monetary analysis indicates that the growth momentum of economic activity, as depicted by real GDP is likely to weaken visibly in the months ahead. Given the possibility that the micro-foundation of the U.S. economy is severely dislocated on account of the previous aggressive lowering of interest rates by the Fed, it will not surprise us if the economic slowdown is going to be much more severe than what we currently envisage.

Link here.LOWEST RATED JUNK BOND SALES AT RECORD LEVELS

U.S. companies one step away from default are selling a record amount of bonds. Jostens Inc., the biggest maker of school rings, is among borrowers rated CCC or lower who have sold $20 billion of debt since December. The sales are the most since at least 1999, when Bloomberg began compiling the data, and are four times the amount from a year ago. Investors are buying the worst-rated junk bonds on speculation the fastest economic growth since 2003 will keep default rates near historical lows.

Bonds rated CCC by Standard & Poors are in the lower half of non-investment grade. S&P describes them as currently vulnerable to nonpayment. They yield an average of about 11.3%, or 616 basis points more than Treasuries - the narrowest since 1997 - Merrill Lynch data show. A year ago, the debt yielded 11.8%, a premium of about 733 basis points. A basis point is 0.01 percentage point. The narrower spread saves a company about $1.2 million in annual interest on every $100 million borrowed. The spread between the lowest-rated junk bonds and other high-yield, high-risk debt is also narrowing. The gap shrank almost a full percentage point in the first quarter to 303 basis points, Merrill data show.

Sales of CCC and lower-rated bonds are increasing faster than other high-risk, high-yield bonds. Overall junk bond sales increased only 1.5% to $43.5 billion in the first three months of 2006, Bloomberg data show. Generally it takes about two years for poor-quality companies to hit the wall, said Margaret Patel, senior vice president and portfolio manager of $7 billion in high-yield debt at Pioneer Investment Management in Boston. There is a big appetite for lower-rated paper because risks still seem low. Patel said she has not purchased CCC rated bonds in the past year because she is concerned about potential defaults even as the nonpayment rate remains below its average over the past 25 years. She declined to be more specific about her holdings. Chris Cordaro, who helps manage $1.3 billion at investment adviser RegentAtlantic Capital LLC in Chatham, New Jersey, is also avoiding CCC rated junk bonds, he said in an interview yesterday. Investors dont get compensated for the risk, he said.

Even CCC rated companies considered in so-called technical default, meaning they asked investors to revise the terms of their debt, were able to sell bonds in the first quarter. Level 3 Communications Inc., a Broomfield, Colorado-based long-distance phone operator, entered technical default in January by asking investors to extend debt maturities. Charter Communications Inc., the cable company controlled by Microsoft Corp. co-founder Paul Allen, asked investors in August to swap their bonds for longer-term debt to help conserve cash. The request placed the company in technical default. In January Charter sold $450 million of debt rated Caa1 by Moodys and CCC- by S&P.

Link here.THE INSTABILITY OF STABILITY

Stability is Unstable, Jim Grant asserts. Low volatility is, ultimately, the source of high volatility, he writes. Tranquility emboldens investors, speculators and traders to take more risk and they would otherwise do. Then something from the blue say, a Russian default shatters the peace, and the leveraged and overextended operators trip over themselves trying to raise cash, even those operators whose resumes include the Nobel Prize in economics Grant refers, of course, to the meltdown of Long Term Capital Management, whose payroll included a couple of Nobel Prize winners. But he also recalls this infamous event for a more significant reason. Measures of bond market volatility are as low today as they were in 1998, immediately prior to the LTCM disaster. The Treasury market is as still as a statue, Grant relates, If loitering were a crime under the securities laws, the government yield curve would be under arrest.

But Grant does not welcome this tranquility. The junk-bond market is a laboratory in the baleful effects of peace and quiet on the pricing of risk, he explains. [Note: See article summary immediately above.] Stability at very low interest rates is especially dangerous. Just by reaching for yield, investors encourage more companies to issue more debt. The higher and more insistent their reach, the lower the credit quality of the issuance. Before you know it, the new bond crop is blighted by rising defaults. Whereupon, credit spreads widen and CDS prices climb. Volatility has not departed the financial markets entirely, as the frenetic recent trading action in the commodities markets attests, but it has taken a lengthy sabbatical from most corners of the U.S. bond market. Narrowing interest rate spreads also testify to the serenity that has descended upon the bond market. So fearless are bond market participants that they now accept near-record-low yields for high-risk bonds. Credit default swap (CDS) prices have also drifted to shockingly low levels. CDS are the default insurance of the bond market. When anxiety is high and complacency is low the price of this insurance rises. And the reverse. Today, CDS prices are as low as they have ever been. In short, bond investors fear no evil.

While it is certainly true that volatility may continue to fall for a while, the odds would seem to favor the opposite course. Buying volatility, therefore, would seem a reasonable risk/reward proposition. Buying volatility, however, is not simply a bet on mean reversion, or on mathematical probabilities. It is a hedge against unforeseen risk. Because volatility expands during episodes of rising fear or panic, the owner of volatility benefits when anxiety increases. But even if one knew the appointed hour when volatility would return to the bond market, preparing to profit from the event is no small matter. Grant advises buying CDSs on a basket of bonds. But he readily concedes that the average individual investor would find it impossible to put on the trade.

However, a couple of approximate substitutes exist. Several newly minted mutual funds seek to profit from a drop in bond prices (rise in yield). Rydex Juno, the granddaddy of short-selling bond funds, profits whenever the price of the 30-year Treasury bond falls. As such, Juno can be counted on to prosper during an all-encompassing rout in the bond market. But since the greatest excesses in the bond market reside in the corporate sector vs. the Treasury sector bearish bond investors might wish to focus their attention on corporate debt securities. For example, the iShares GS$ InvesTop Corporate Bond Fund (NYSE: LQD) is an ETF that tracks an index of investment grade corporate bonds. The bearish investor could either sell short this ETF or buy long-dated put options on it.

Taking higher risks, one finds the Flex Bear High Yield Fund (AFBIX), which provides a direct play on shorting corporate junk bonds. This open-end mutual fund actually does what Grant advises: it buys credit-default swaps. Specifically it buys CDS on the Dow Jones CDX North American High Yield Swap Index. For the last several years, as junk bond prices have soared, buying CDS has not been a terrific idea. But in the less tranquil world that Grant anticipates, they may prove to be a fine item to own. As Grant points out, The odds of an outlying event do not change just because the market is complacent. Nor do the odds change because the cost of insurance is very low. Maybe it is time to take out a policy.

Link here.How to make a bet against continuing stock market complacency.

Todays stock market is a vast repository of hard financial data and soft human emotions. At extremes, human emotion counts more than hard data. As investor sentiment oscillates between extremes of greed or fear, share prices soar or sink. Lately, stocks have been soaring, both here at home and abroad. As a result, most measures of investor sentiment are registering high levels of confidence and complacency the very attributes that often presage important market peaks.

Investors who fear the near-term fate of the U.S. stock market, therefore, may avail themselves of a new index option from the Chicago Board Options Exchange. A few weeks back, the CBOE issued a new series of options on the VIX Index. (This index is also known as the fear gauge. To learn more about it and the new VIX options, click here.) These options provide a very novel way to hedge against an overdue stock market correction. More than two years have elapsed since the last time the S&P 500 slipped more than 10%. Such tranquility has fostered widespread complacency, as evidenced by the VIX Index itself. At a reading of 11.13, the VIX languishes very near its all-time low. In other words, investor fear is near an all-time low. For perspective, the VIX ticked above 14 as recently as January, and soared above 40 twice in the last 5 years. In other words, 11.13 is quite low indeed. An anxious investor, therefore, could purchase call options on the VIX and hope for a meaningful stock market correction.

The low VIX reading is not the only hint of investor exuberance. Several global equity indices provide additional hints: The Nasdaqs 5-year high, the Russell 2000s all-time high, the Russian stock markets all-time high, the Indian stock markets all-time high and the rapidly expanding population of all-time highs elsewhere around the globe. Back here at home, bullish sentiment has approached rare extremes. The 10-day Daily Sentiment Index (MBH Commodity Advisors) last week hit a sky high 86.6% Bulls, notes options pro, Jay Shartsis. In the near 20-year history of this survey, only eight days have reached a greater bullish extreme. This is a good piece of bearish evidence. Adding to the growing body of bearish indicators, Shartsis notes, Over the past six months, the Dow Jones Utility Average is down 10%, while the broad market has been rising. One study looks at past experiences when the utilities were down at least 10% over a six-month period while the S&P 500 was up at least 5% over that time span. Going back to 1950, there were only five such occurrences Over the following three months, the S&P 500 lost on average 8.4%. That is an eye opener. The crash in 1987 was preceded by one of these divergences as was the grand top of March 2000. These divergences carry on for what seems like a long time to people who watch the market every day. The broad market just soldiers on and it doesnt seem to matter, until the day comes when it does matter.

Perhaps that day is fast approaching. Many of the worlds equity markets are priced for perfection, and most investors seem to anticipate continuing perfection. We do not. But neither do we anticipate extreme imperfection. We merely observe that U.S. share prices are relatively high and that the VIX Index is relatively low. Therefore, the price of betting on imperfection has rarely been lower. An August 15.00 call option on the VIX Index costs about $1.25. That is not exactly cheap. But neither does it seem so expensive when one remembers that the VIX never dipped BELOW 15.00 in 2002, 2003 or 2004.

Link here (scroll down to piece by Eric J. Fry).IN RUSSIA, A WARNING OF IRRATIONAL EXUBERANCE

Russian stocks, buoyed by high oil prices and a surge of foreign investment, have been soaring. After an 83% gain in the RTS stock index last year the best stock market performance outside the Middle East in 2005 the index is up nearly 33% so far this year. That market boom has multiplied the already apparent signs of wealth in the Russian capital. A Lamborghini dealership has opened. Airline travel has picked up. A trade fair for companies aimed at millionaire customers came to Moscow.

Amid the optimism and enthusiasm, one man is striking a discordant note. Oleg V. Vyugin, Russias top market regulator, has repeatedly taken to issuing dour warnings. Recently he has cautioned that the Russian market is showing some alarming signs of become too expensive compared with other emerging markets that have been the darlings of global investors for the last year. Russia was considered a desirable object for investment, he said. This drove the market up. But that flow will not last forever. Institutional investors, he noted, have already snapped up most of the bargains in oil, telecommunications and consumer companies. Future growth will come slower, he cautioned. Mr. Vyugin emphasized that he did not believe that the stock market was overheated or overvalued relative to the profitability of the companies listed. Rather, he said, the potential problem lies in the volatility of the huge flows of money from Western emerging-market funds. Foreign money, he said, flows in and it will flow out.

Emerging markets from Asia to South America have done very well for institutional investors in the last year, and Russia has been a particular favorite. In the first three months of this year, through March 29, investors put more than $3.4 billion into Russia out of a total flow to emerging markets of $24.2 billion, according to Brad P. Durham, managing director of Emerging Portfolio Fund Research, a company based in Cambridge, Mass. Russias weighting in global emerging market funds, known as GEM funds, rose from 4% at the beginning of 2005 to 6.6% at the end of the year, he said, indicating growing interest compared with other markets.

Mr. Vyugin, 53, a lanky, bespectacled man who wears drab charcoal suits and has a shock of unruly gray hair, seems to relish the role of reclusive naysayer in a garish boomtown. Analysts praise his grasp of economics and staid mannerisms, and take his past as a Soviet-trained mathematician as a sign of intellectual rigor. In a city of scandals, intrigue and overnight fortunes, where businesses are sometimes raided by masked gunmen, Russia may need a market regulator who by his own admission rarely leaves his apartment except to go to work, they say.

Russia passed an obscure but important barrier this year, Mr. Vyugin and analysts say. For six years after the economic crisis of 1998, Russian companies traded at a price-to-earnings ratio that was lower than those for most other emerging markets. Now, Russia is projected to trade at a ratio of 13.3 in 2006, compared with an average of 12.3 in emerging markets, according to calculations by Mr. Durhams company. Still, Peter Westin, an economist at MDM Bank in Moscow, said Russian companies do not look overpriced compared with Indian and Chinese companies. We might be getting into that period, but were not there yet, he said.

Back in the office of Mr. Vyugin, the regulator, he said that for now oil prices and United States interest rates were working in Russias favor. His warnings, he said, were meant only for new private investors in Russia who risk buying in at the top of the market. He switched into English briefly to recall Alan Greenspans caution against irrational exuberance. Then he glumly admitted he did not think his warning would have much effect. I cant teach brokers whether the market is overheated, he said. They know better than us, I hope.

Link here.WHEN JAPAN TILTS, ICELAND QUAKES IN INTERTWINED GLOBAL MARKETS

When the Bank of Japan shrugged, Icelands financial markets tumbled. The worlds second-biggest economy became entwined with an island of 300,000 people as hedge funds borrowed in Japan, where the benchmark interest rate is 0.15%, and used the money to buy AAA-rated Icelandic bonds paying 9%. Speculation that the Bank of Japan would begin raising rates, confirmed March 9, caused investors to unwind these so-called carry trades. The markets are coming to grips with the expectation that Japan and other central banks will start raising rates,qsays Robert Sinche, head of global foreign exchange strategy at Bank of America Corp. in New York. As the process unfolds, you uncover certain fault lines and they usually arent where youd expect them. Maybe Iceland was the first casualty.

Iceland is particularly vulnerable because the government and Alcoa Inc. have poured $2.5 billion, 16.5% of last years GDP, into aluminum production projects during the past two years, stoking inflation and pushing up interest rates. The Icelandic krona has dropped 11.8% against the dollar this year. The krona rose 63% in the four years through December 31 as economic growth accelerated to 6% and investors bought Icelandic assets. Now, spooked by a widening trade deficit and rising interest rates elsewhere, many investors are selling. The currency weakened and yields on Icelands bonds climbed after New York-based Fitch Ratings cut its outlook for the country on February 21, citing rising international debt and a current-account deficit that reached 15% of GDP last year. The currency had gotten overvalued, says Donald Quigley, who helps manage about $2 billion in bonds for Bank Julius Baer & Co. in New York. Quigley cut his Icelandic positions he declined to say how large they were by 95% this year.

As demand for Icelandic assets cools, economists at ING Financial Markets in London forecast the krona will weaken to 80 to the dollar within six months, from 71.61 on March 31. It reached a high of 59.50 on November 2. The currencies of New Zealand and Hungary, two other economies with fast growth and widening current account deficits, are also vulnerable. The New Zealand dollar has dropped 9.9% against the U.S. dollar this year, trading for US$0.6157 on March 31. The Hungarian forint has fallen 2.2% and now trades for 217.88 to the dollar.

Declines in New Zealand and Hungary are not likely to spread further, unlike crises that began in Mexico in 1994, Thailand in 1997, Russia in 1998 and Turkey in 2001, says Cian Walsh, who helps manage about $1 billion of emerging market debt at BlueBay Asset Management in London. Countries such as Russia, Brazil, Argentina and Thailand are running current account surpluses thanks to Chinese demand for their raw materials. Iceland is a highly leveraged economy, Walsh says. The people who got involved were very short-term investors. Its a tiny market, and the whole story has been hugely overdone. Its unlikely to affect other markets from now.

The Bank of Japans decision to end a five-year policy of fighting deflation, opening the door for rate increases later this year, helped damp investor appetite for Icelandic bonds. The banks March 9 announcement, which had been signaled for weeks, followed two rate increases by the European Central Bank, its first in five years. The possibility that Japan will raise rates triggered the selling of Icelandic assets, says Mohamed El-Erian, who runs Harvard Universitys $26 billion endowment. The minute a few people try to get out of a technically crowded trade, everybody tried to get out. While there is still a wide spread between Japanese and Icelandic interest rates, it is likely to narrow. The focus is moving away from interest-rate levels to interest-rate directions, says Philip Wee, senior market strategist at DBS Bank in Singapore.

Carry trades involving the dollar and yen have been popular among hedge funds for the past decade. With interest rates almost zero in Japan, investors could borrow there and put the cash to work in the U.S., gaining from both the 3-plus percentage-point difference in yields and the dollars rise against the yen. The last big unwinding of carry trades was in 1998, when Russias debt default and the implosion of John Meriwethers Long-Term Capital Management LP sent the yen, which had been weakening since mid-1995, surging 20% in two months. The largest hedge funds at the time, Julian Robertsons Tiger Management LLC and George Soross Quantum Fund, both lost money as the dollar dropped to 113.60 yen at the end of 1998 from a peak of 147 on August 11. Soros, now 75, became famous in 1992 after he made $1 billion betting that the British pound would fall after the government abandoned sterlings peg to a basket of European currencies. He did not use carry trades in those transactions.

Link here.HOW MANY BUBBLES BEFORE THE FATAL ONE?

There is a well known old saying Nothing succeeds like success. There is another perversion of that saying: Nothing succeeds like excess! As the globes economies cross from Winter into Spring in this year 2006, there is virtually no area not enjoying prosperity and success. Economic success, as usually described by pundits and media always encompasses the word growth. Virtually in every instance growth in any economic form relates to profits. Obviously, profits are success in this early 21st century. Much of the world measures these profits in U.S. dollars.

For much of the last four years, this growth or expansion has been fueled by the most incredible growth in global liquidity in the known annals of human history. Not only has there been enormous liquidity, interest rates have been phenomenally low until very recently. Admittedly, the U.S. Federal Reserve has spent over a year raising the overnight rate in the United States from 1% (below 0% on an inflation adjusted basis) to the current 4.75%, but the longer end of the curve has virtually ignored their efforts. Liquidity during this Federal Reserve charade has mounted. In the case of the broadest measure (to be extinguished with this months last report for reasons unexplained by the Fed) M3 has advanced at rates approaching 10% in recent months. In passing, it might be noted that the required contribution by financial institutions of the components of M3 to the Federal Reserve are to be continued, but the Fed just does not want to publish this revealing measure any more.

One of the most prolific areas of growth globally has been real estate, particularly residential real estate. With interest rates at epochal lows around the globe, the old adage in real estate of low rates equals high growth has been exploited to the utmost. Much has been written about this munificent growth in houses and house prices and, other than a canary in the coal mine story about one small country sucked into the orgy, this will not concentrate on that aspect of liquidity and credit growth, but on other manifestations.

First to get the afore-mentioned housing related bubble story out of the way we would initially mention a central bank today forced to raise its interest rate equivalent to our Fed funds rate to 11.5%! That beleaguered central bank is the central bank of Iceland. This miniature country got caught up in the house prices only go up mantra as their relatively high interest rates attracted a tsunami of liquidity which poured into you guessed it the housing market. As more houses than Icelanders emerged, the market flooded and the tsunami went back out to sea, leaving the Iceland kronor down some 20% in a couple of weeks. How the story will play out, we have no idea, but there is at least a lesson to be learned for possible other liquidity driven booms, bubbles and housing explosions for the near future. The same hedge fund driven carry trade that caused this Icelandic meltdown (technical term) is besetting the New Zealand kiwi, recently forcing their short term rate to over 7%. As these hedge fund games unravel, some serious damage will be done to small, innocent countries. Since there has been a residential property bubble, in each instance, the commercial banking systems, in which most mortgages reside in these small countries, will confront increasingly difficult credit quality, default, foreclosure and bankruptcy situations. This may possibly lead to severe damage or crisis in the banking systems involved.

Now we proceed to the main point of this exercise. It is our contention that The World of Credit Extension has changed dramatically since the last significant test of credit during the 1989-1991 slowdown (the 2001 drop was so slight as to have not been a test of underwriting and delinquency in our opinion). We will attempt to catalogue some of the more significant of these changes. There are so many that detailing the whole universe is impossible. My friend, Doug Noland has made the point for an increasing number of years now that the definition and nature of Credit has changed completely from what most still assume it to be.

What is endlessly fascinating is how little this transmogrification is understood at this late stage of the game. Doug first showed that the conventional central bank creation of credit definition was outmoded quite a few years ago, using as an example, the Government Sponsored entities Fannie and Freddie. These two Agencies were able to create virtually unlimited amounts of credit through the belief that they were governmentally supported and an accommodating financial market without any interaction with the reserve based banking traditional method of credit creation. In 2003, they essentially restarted the economy after the blow-up of the dot-com/telecom bubble through easy credit to a housing sector emboldened by Fed rate cuts to levels which could not be resisted, both in the refinance and the construction arenas of residential housing. Too bad it turned out that these supposedly pristine, superbly managed entities were really cooking the books! Nevertheless, they have several trillions of assets now, and even more trillions of indirect exposure through guarantees of mortgage debt.